At the 4th Annual PROENERGY Conference, held in Phoenix, AZ in January, the mood was buoyant. Gas turbine (GT) orders (and shop reservations) are skyrocketing, electricity demand growth is higher than it’s been in decades, hyperscale data centers and their insatiable need for electricity are being built and planned throughout the country, and restrictive regulatory regimes, at least at the federal level, are being relaxed.

Several speakers seemed to bask in the glow of that phrase characterizing the digital revolution: “Move fast and break things,” originally coined, or at least attributed to, Mark Zuckerberg, founder of Facebook, now part of the digital behemoth and hyperscale investor, Meta.

However, percolating just below the giddiness over the prospects of phenomenal growth were the real constraints of infrastructure businesses like electricity production and delivery. After all, as one panelist said, IT systems depreciate in a few years. Electricity infrastructure is planned on a 20–50-year time horizon. Additionally, explosive growth poses its own inherent challenges, and the keynote speaker, and a host of panelists, were not shy in addressing them.

Surge or bubble?

The venerable Mark Axford, Axford Turbine Consultants, headlined the conference by juxtaposing two words for the state of the market, surge or bubble, and then emphatically answered, Surge!

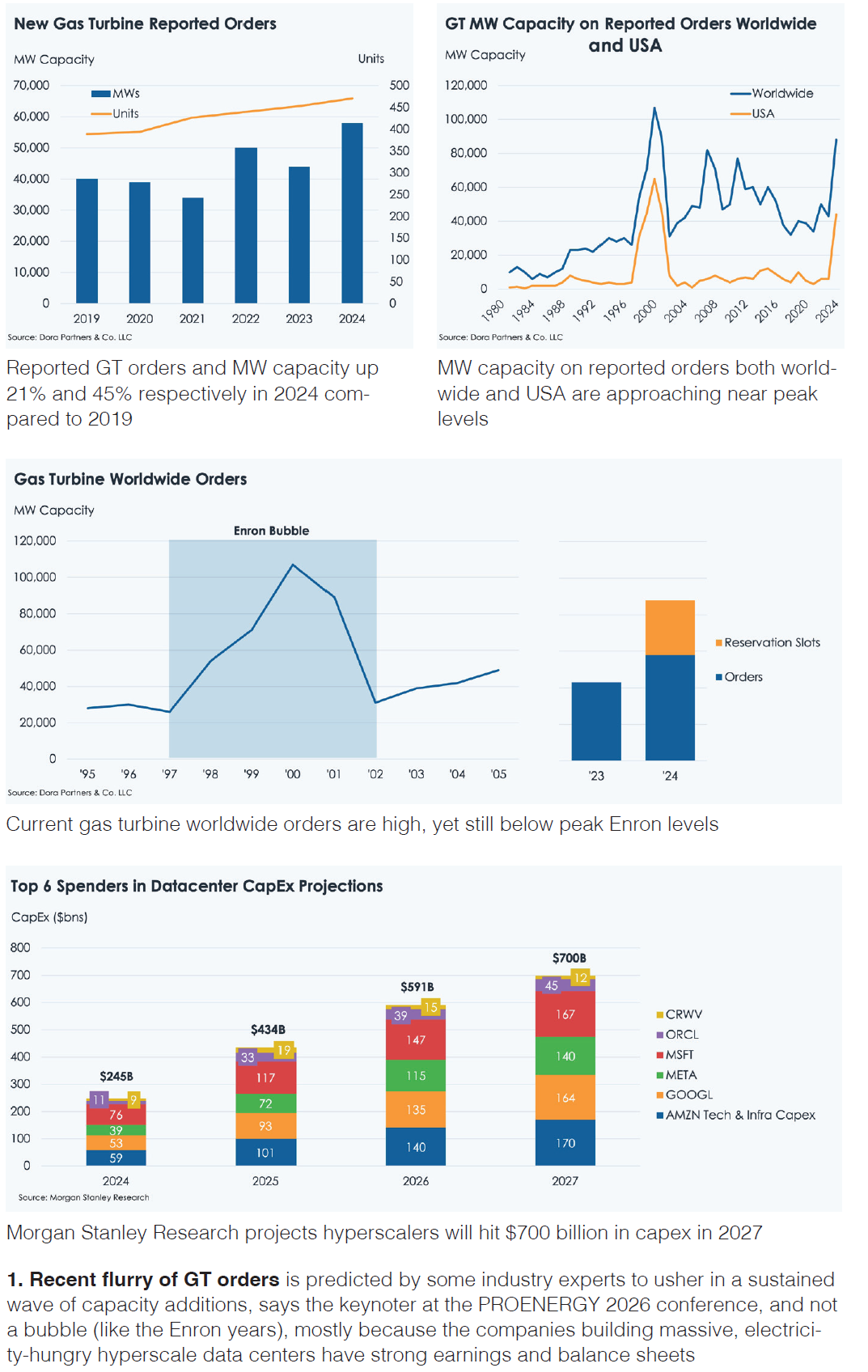

The numbers Axford put up are breathtaking (Fig 1). At least one GT manufacturer expects demand to exceed 100 GW/yr worldwide from 2026 to 2035. For context, that’s a decade of orders at the same rate as the peak of the last period of manic GT orders, 1997-2001. Axford cautioned that sustaining peak-cycle ordering rates for a full decade is unlikely, given the many variables that can disrupt demand and project execution.

Adding to the upbeat outlook, consolidation is reshaping the owner/operator landscape as major fleets are getting bigger, with players like Constellation absorbing large GT operators such as Calpine. At the same time, new OEM entrants from Korea are moving into the market, while big dogs like GE Vernova and Siemens Energy are ramping manufacturing capacity at speed.

Meanwhile, Axford continued, huge hyperscale data centers are getting built. As an example of what hyperscale means to the electricity production side, the $15-billion Stargate AI data center outside of Abilene, Texas, will have 39 LM2500 Xpress simple-cycle units and five Solar Turbine Inc units. $500-billion worth of other Stargate sites are being planned and built in other locations around the country.

The second “big deal” project Axford highlighted is the $10-billion, 4500 MW combined cycle facility on the grounds of the former coal-fired Homer City powerplant in western Pennsylvania. All the output is expected to be consumed by data centers, not by the PJM grid. Homer City will comprise seven 7HA.02 GTGs and seven steam turbine/generators.

Third project highlighted is the $20-billion “Colossus” project on the Tennessee-Mississippi border near Memphis. Phase 2, now underway, will include six PROENERGY PE6000 units along with eight Solar Titan 350 units and other smaller Solar units.

One thing that makes this a surge, not a bubble like the dotcoms of yore, is that the AI digital firms are well-capitalized and are funding the build-out from revenues, Axford noted. As if to redefine the word, uptick, Axford revised an earlier uptick of 7-10% in GT order growth for 2025 to 22%! It’s good to be wrong in the right direction.

What might alter that direction? Axford lists Sparc architecture (scalable processors), low power chips coming onto the market, invasion of Taiwan (where much global chip-making capacity resides), new regulations on the AI industry or electricity, and political upheaval in the US. It’s an AI arms race, he concluded.

Temper, temper

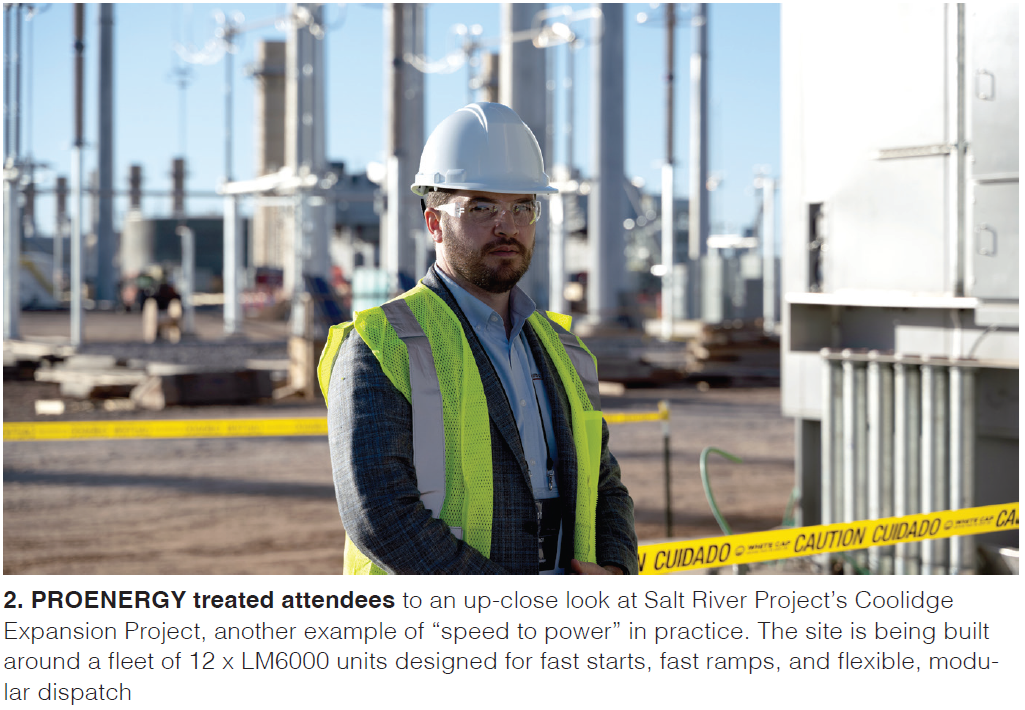

What does all this mean for one of the largest public power companies (and the largest raw water supplier) in the US? Well, according to Bill McClellan, Salt River Project (SRP), it means SRP is planning to double its installed capacity within a decade. “It took us 100 years to build our first 13,000 MW,” he noted. SRP is adding capacity “at an unprecedented rate,” an example being the addition of 12 LM6000 units at its Coolidge site, which already has 12 LM6000s (Fig 2). The public utility already has approval to add 6000 MW.

He tempered the optimism a bit by reminding the audience of the development risks involved, among them: Building the associated transmission; supply chain issues (noting step-up transformers as an example); tariffs/tax credits, labor costs (and rising costs “across the board)” gas supply constraints in certain areas (SRP’s territory is one); regulatory uncertainty; and community opposition of which there is a “tremendous increase across the state [of Arizona].”

Panelists in the following business roundtable, “Evolving Power Demands,” elaborated on many of these risks and opportunities (Fig 3). Speakers included: John Adams, Crusoe (powerplant developers for the Stargate facility mentioned above); Tyler Kopp, Energy Capital Partners (ECP, private equity investor and majority stakeholder in PROENERGY); Dylan Bearce, Tucson Electric Power (owned by Canadian firm UniSource); Kim Flowers, NavEnergy (coal operations on the Navajo territory); and moderator Landon Tessmer, PROENERGY.

Out with old definitions

Tessmer started them off with what was perhaps a rhetorical question, has the definition of “bridge technology” (which had referred to GTs as a bridge to a sustainable future) changed? The answer was unanimous: Cycling GTs were, just a few short years ago, considered the “backbone” to stabilize intermittently available capacity from renewables, but they are now the bridge to “grid catch up” and “speed to baseload capacity expansion.”

Some of the rhetoric did echo earlier GT booms. A major GT supplier in the 1990s used to offer a Pro Gen scheme (progressive generation) – build simple cycle, expand to CC, and add a coal gasification plant if necessary (and as a hedge on gas prices). That strategy, of course, might have looked good on paper to executives with little engineering and regulatory experience, but was impractical for many reasons. No one needed it besides because the natural gas “scarcity” and emphasis on “clean coal” technologies of that period was replaced by a natural gas glut.

Adams noted that simple cycles are being built now for speed to capacity, but “combined cycles will be added later.” Hydrogen and/or carbon capture are now playing the role of gasified coal, options available should the regulatory regime demand ultra-low CO2 emissions. Flowers mentioned the responsibility to “future-proof asset decisions,” and Adams the concept of “adding in the flexibility for H2 firing and CO2 capture.” However, Kopp noted that CO2 capture rates ding the financial structure with a $15/Mw-hr premium and H2 in GTs in the US “does not pencil in.”

From an operational perspective, H2 combustion is “different,” Bearce observed, and requires different combustor tuning techniques. “It’s a contingency piece,” he noted.”

Obstacles mount

Adams described the current climate as “the hottest market he’s seen in forty five years in the business,” “we can’t get GTs fast enough for 2029 and 2030,” and “it’s going to be crazy for the next five years,” sentiments echoed by Kopp who said AI companies “are the best capitalized firms on the planet.” Nevertheless, the obstacle course was evident from panelists’ remarks.

Water. Adams said there’s been a huge refocus on water, and commitment to net zero water consumption or even water production at hyperscale data centers. Bearce noted that there are “ways around water [constraints], but costs escalate.”

Transmission. Flowers conceded that you can’t have generation without transmission and that land issues and routing are “so complicated.” Bearce added, transmission costs have to be spread across the customer base. He also mentioned load pockets, land availability, and public opposition: “Contingency analysis is not just N-1, there are lots of guesses involved.” “We need much more engagement with customers,” he continued, “there are lots of balls in the air with respect to public perception.”

Overall implication: Expanding transmission is not necessarily compatible with “speed to power.”

Labor. Adams listed two critical challenges. One is the lack of workers in the US currently. “We are 250,000 laborers short,” he lamented, “we need 80,000 electricians alone!” That could bite even harder at a time of severe restrictions on immigration. “How do we make construction work ‘sexy,’” he queried, “an electrician can make $200K annually today!” Labor is related to the other challenge, cost inflation: “EPC costs have doubled over the last two years,” Adams stated. However, data center revenue “can easily cover those costs.”

Lack of gen options. Supporting the “surge” conclusion is the lack of other generation options. No one is yet talking about a return to coal (although coal plants take much longer to build). Tessmer did ask the panel about small modular reactors (SMRs), but they were roundly dismissed, at least for the short term. Some of the commentary: Viable technology is at least five years away, the US has no repository for spent fuel, regulatory framework does not support the size, and the technology is not compatible with “speed to power.” Large scale batteries, even with costs coming down, have one big limitation: They supply no inertia to the grid.

Fuel supply. Access to natural gas resources is critical, which is why Texas and Pennsylvania are such hot regions for power plants and data centers. Tessmer noted that “50% of our quotes for LM6000s request dual-fuel capability.” Adams stressed having two sources of gas at the site. Dylan mentioned the premiums incurred for flexibility in long-term gas delivery. “But they are worth it,” he stressed. It is costly to have diesel-firing backup “just sitting there,” Adams bemoaned.

The “nines.” Reliability requirements for data centers were another eye-opener. Where once digital companies talked about “five or six nines” for power quality, their sights have lowered to 99.9%. Flowers noted that data centers must plan for curtailments. Adams stated that you need 1000 MW of batteries for 1000 MW of electric supply. Also, lots of smaller GTs present better N+1 reliability than a few large units. Synchronous generators can also play a role.

Almost inconceivably, data centers can experience demand swings of up to 100 MW per nanosecond. As such, they pose a quantum leap in reliability challenges, offering opportunities for fast response batteries and flywheels behind the meter. Such dramatic load swings can cause failures in GTGs, too.

Analytics, outages, people

Three critical themes emerged from the Operational Challenges panel: more and better use of data analytics, new approaches for outage management, and finding, retaining, and training site workers. Panelists were Scott Smith, TC Energy; Brian Palmer, FM Global; Paolo Rocha, Silicon Valley Power; Cory Anderson, PROENERGY; and moderator Lance Herrington, PROENERGY.

“Is the intermittency factor following renewables over- or understated,” asked Herrington, to kick it off. Understated, answered Palmer immediately. Anderson noted that machine inspections get harder to manage, complicating risk-reward decisions. Smith mentioned that it’s harder to find parts for peaking plants. All agreed that new ways forward were needed for managing outages, such as relying more on condition-based assessments, less on calendar-based planned downtime, and shifting work from majors to minors to avoid the industry crunch of typical spring and fall outage periods.

Following a more general question on getting better at maintenance, Rocha noted that even having a spare turbine for a 2-unit LM6000 combined cycle isn’t adequate for reliability. Units go into depots for 12-18 months these days, he continued.

Palmer and Smith proved to be big champions of predictive analytics to inform risk-based decisions. Smith went further, asking can we deploy AI for better modeling and predictions of machine health and potential component issues, and better use of analytics in business planning. Herrington emphasized an opportunity for the industry to standardize on how borescope inspections are conducted, and for O/Os to “bring all the prediction data together in one place. Yes, agreed Palmer, data is still reviewed “in silos.” More collaboration among owners, operators, service providers, and insurers would help.

Rocha called the “people aspect of operations” a “terrible” issue for them. “We are in an area with an exorbitant cost of living and have a huge problem attracting talent.” Palmer reiterated what most should know: Equipment losses are often driven by poor operator decisions.

Coming down the pike…

PROENERGY execs asked that most of the details divulged in the R&D session not leave the room, but one headline, in particular, is in order:

- The new PE6000 engine has been successfully validated and 20 units have shipped. Fleet leader has 750 starts and 4235 hours; fleet totals are 3741 starts and 27,384 hours. CCJ